** 02-Jun-2021 World View: Copying text

Higgenbotham wrote: Wed Jun 02, 2021 12:33 am

> From reading the news, the explanation for the increase in the use

> of the reverse repo facility is, with the end of the SLR

> exemption, banks reduced treasury holdings. As a result, some

> banks are turning away deposits. That cash is being redirected

> toward money market funds and they are parking it in the reverse

> repo facility for lack of better alternatives.

> Bloomberg is automatically limiting the amount of text I can copy

> out of the article, so I did the above summary and the entire

> article can be read here:

>

https://www.bloombergquint.com/gadfly/f ... verse-repo

Yikes! I don't have that problem, since I run with javascript turned

off as much as possible. I use the "noscript" addon to Firefox

which is incredibly good, since it gives me a lot of control.

I can't stand running with javascript on. It seems that every page

has all sorts of unwanted popups and other blinking crap apparently

targeting teenagers. I've recently also begun using the "DOM Delete"

addon which lets you delete various garbage elements on the page, even

when javascript is turned on.

Another possibility if you want a text copy of a page, might be

to print the page to a PDF file, open the file in Acrobat, and

use "Save as text ...". That might or might not work.

If you have to convert to text often, there are online OCR services.

Several years ago I purchased the Omnipage program, which was

expensive, which I use all the time. But I think now they've turned

it into a SaaS, which I don't like.

Anyway, here's the text from the Bloomberg article you referenced. I

also including links to the images in the article, although the images

may or may not be displayed since Bloomberg doesn't like that:

The Fed Is Mopping Up Its Own Mess in Reverse Repo

Brian Chappatta

May 28 2021, 8:01 PM

May 31 2021, 5:35 AM

(Bloomberg Opinion) -- Over the past couple of weeks, I’ve been

tweeting near-daily updates of the following chart, which shows the

amount of cash placed at the Federal Reserve’s overnight reverse

repurchase facility. Use soared to a record $485.3 billion on

Thursday, capping an unprecedented surge: The Fed Is Mopping Up Its

Own Mess in Reverse Repo

The account balance has been declining as the Treasury disburses

fiscal aid to fight the Covid-19 pandemic and prepares for the debt

ceiling to come back into play later this year. Often, as was the case

recently with stimulus payments to state and local governments, that

cash makes it way into money-market funds, which then need to invest

it somewhere. As the previous look at front-end rates clearly showed,

reverse repo is an obvious choice.

Treasury’s swift reduction in its cash balance shouldn’t have

surprised anyone. I wrote in December that short-term rates were

headed for zero and that the Fed might have to intervene, perhaps by

selling short-dated Treasuries outright to counter a decline in bill

issuance. Yet the central bank hasn’t done much to tweak its bond

purchases, which are advertised as a way to provide accommodative

monetary policy on top of near-zero interest rates and won’t be

touched until the economy makes “substantial further progress.” Policy

makers chose not to shift the buying away from the front end, knowing

what was coming down the line.

Another problem with barreling forward with bond buying on autopilot,

as was made clear during March when markets were fretting about the

supplementary leverage ratio, is that it’s overwhelming some of the

biggest U.S. banks. They don’t want any more reserves because it means

they need to hold more capital, but that’s exactly what happens when

the Fed is adding so many assets to its balance sheet (reserves at the

Fed are the offsetting liability).

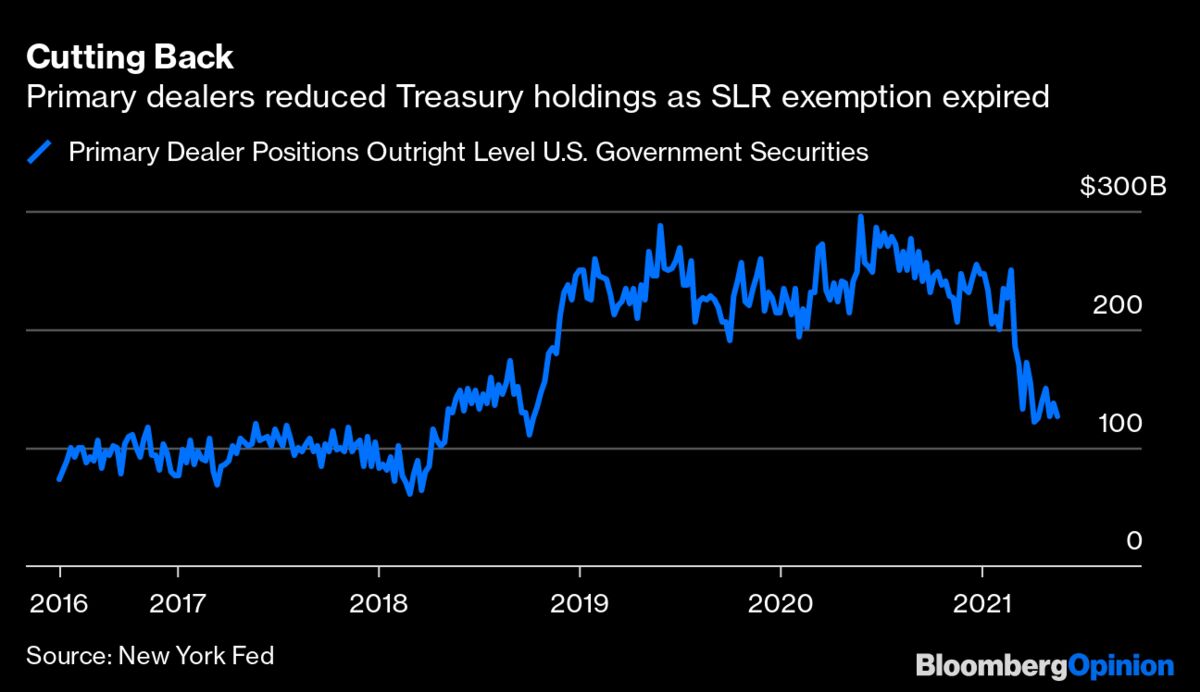

So, naturally, the only thing left for primary dealers to do was to

scale back on their Treasury holdings: The Fed Is Mopping Up Its Own

Mess in Reverse Repo

Again, this was the natural result of ending the SLR exemption. I

wrote in March that it looked as if the Fed was trapped, suggesting

that perhaps a middle ground would be allowing reserves and Treasuries

accumulated during the pandemic to be exempted. Instead, policy makers

opted for a clean break, even as bankers like JPMorgan Chase &

Co. Chief Executive Officer Jamie Dimon raised the prospect of these

regulations forcing them to turn away deposits.

It wasn’t an empty threat: reportedly some banks are doing just

that. That cash instead gets redirected toward — you guessed it —

money-market funds, which need to invest it somewhere. Yet again,

there’s the Fed’s reverse-repo facility ready to absorb it. As of

mid-March, it increased its limits to $80 billion per counterparty

from $30 billion. It “reflects the growth and evolution of U.S. dollar

funding markets since the limit was last changed in 2014.” On

Thursday, the Fed added two more money-market funds to its approved

list, from T. Rowe Price Group and Vanguard Group. Fidelity

Investments has 11 funds that are reverse-repo counterparties. Even

quant pioneer Dimensional Fund Advisors has one.

It’s unclear whether the Fed can do much to slow this pickup in the

use of its reverse-repo facility. It’s also quite likely that central

bankers don’t see it as a problem. Remember, it allows the central

bank to defend the so-called zero lower bound of short-term rates. So

far, it’s accomplishing that task, with the fed funds rate steady at

0.06%. Rather than force even more reserves onto banks, which can’t

make enough loans relative to deposits, persistently huge reverse-repo

operations are a tidy solution to soak up all the cash that’s seeping

out into money markets, especially with funds content to earn nothing

for now.

Still, central bankers might eventually give in and raise the

so-called administered rates that the Fed pays at its reverse-repo

facility and on excess reserves (IOER). The fact that they haven’t yet

done so potentially suggests some concern about the optics of raising

rates, even if it’s for technical reasons. But the prospect of money

funds closing to new investors or offering negative returns, as

suggested by Bank of America Corp. strategist Mark Cabana, might be

seen as enough of a systemic risk to force their hands.

For now, though, the startling reverse-repo chart can be viewed as a

mess created by the Fed that it’s mopping up itself.

This column does not necessarily reflect the opinion of the editorial

board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt

markets. He previously covered bonds for Bloomberg News. He is also a

CFA charterholder.

©2021 Bloomberg L.P. Bloomberg