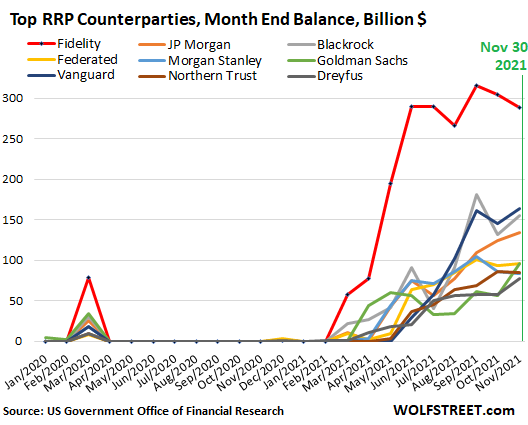

Fidelity’s money market funds,

11 are approved counterparties with the New York Fed.

All combined have been the largest user of the RRP facility.

There have been warnings about turbulence in the weeks ahead as liquidity drains out of the Libor market.

And the real test may come when interest payments become due on U.K. bilateral and syndicated corporate

loans linked to replacement rates, according to James Lewis, a partner at KPMG UK. T

After Rule 2a-7 and Reg T they went comatose. Some.

https://wolfstreet.com/wp-content/uploa ... y-fund.png

Banks want to reduce cash balances and increase Treasury securities on their balance sheet at quarter-end for regulatory reasons.

Banks can deposit their cash at the Fed directly and earn more in interest than with RRPs. On the Fed’s balance sheet, these deposits from banks are liabilities that the Fed calls “reserves,” and it pays interest on them at an annual rate of 0.15%, which is more than the 0.05% it pays on RRPs.

===========================================================================================

Mon Nov 15, 2021 4:42 pm

https://gdxforum.com/forum/viewtopic.ph ... ril#p65769

Series I to Earn 7.12%, Series EE to Earn 0.10%

FOR RELEASE AT 10:00 AM

November 1, 2021

Effective today, Series EE savings bonds issued November 2021 through April 2022 will earn an annual fixed rate of 0.10%. Series I savings bonds will earn a composite rate of 7.12%, a portion of which is indexed to inflation every six months. The EE bond fixed rate applies to a bond’s 20-year original maturity. Bonds of both series have an interest-bearing life of 30 years.

Rates for savings bonds are set each May 1 and November 1.

Interest accrues monthly and compounds semiannually.

Bonds held less than five years are subject to a three-month interest penalty.

thread: Rule 2a-7

Tue Nov 16, 2021 8:49 am it was infered a A Liquidity Crisis is Imminent...

These facts above negate the sentiment as we witness todays reality.

We can only marvel at what we are surrounded by.

Sun Oct 09, 2011 10:55 pm

Against this backdrop what we may be seeing is an unwinding of sweep arrangements prior to the July 21 repeal of Reg Q. As Eurodollar deposits mature, the deposit may be coming back home to the domestic branch in the form of a demand deposit for business accounts, or as an MMDA for accounts owned by individuals. From the Fed's H.8 release we know that there has been a dramatic sudden drop in US banks liabilities to their foreign branches. This is exactly what would happen if Eurodollar deposits were to be brought back to the balance sheet of the US branch. Stone McCarthy

Here is a bare-bones way to think about this situation: A is the customer, B is the service

provider. B informs A what A should buy from B, and a third entity, C, pays for it from a

common pool of funds. Stated this way, the problem has no known economic solution

because there is no equilibrium. There is no automatic balance between willingness to pay

by the consumer and willingness to accept by the producer that constrains and limits the

choices of each.

Functions are mediated as conditions to exist.

Leading Economic Indicators are shifted and so our

pocket we noted was somewhat accurate in nature. Rough number was ~11% deviation mid quarter

in my observation. Time out pockets to sort capital.

As we have seen very recently the rotation is evident on sector sweeps.

https://www.newyorkfed.org/markets/data-hub{kind=link}