You're currently eligible to participate in the Call on Intermediate Securities.

A fully paid lending status report for your Securities account is now available.

https://www.zerohedge.com/markets/nomur ... -implosion

After reporting its biggest quarterly loss since 2009 (driven by losses tied to the implosion of Archegos that were greater than the $2 billion the Japanese bank first reported a month ago) Nomura has decided to suspend or shuffle around several senior employees, including its head of risk.

Fri Oct 16, 2009 6:53 pm

Hubris inflicts lasting pain. Discipline over conviction must prevail or all is lost Washington. The left and the right are wrong.

Since the Consumers is shattered by your historical ineptitude may your creator judge since the honest are afficted and you

deny justice to the common man. So few, for so long have lowered the eyes of honest guidance to indifference. A heavy price

indeed extracted.

https://www.youtube.com/watch?v=V_87AoQaKNw

Financial topics

Re: Financial topics

https://whalewisdom.com/filer/internati ... visers-llc

https://www.zerohedge.com/markets/value ... ating-fund

https://www.ime.usp.br/~sferrari/beta.pdf

https://www.zerohedge.com/markets/value ... ating-fund

https://www.ime.usp.br/~sferrari/beta.pdf

Last edited by aeden on Thu Apr 29, 2021 10:08 am, edited 1 time in total.

Re: Financial topics

** 28-Apr-2021 World View: Signposts Of The End

99% of analyses from mainstream economists are total garbage, as

proven by the fact that they almost always turn out wrong or, at best,

made no forecasts that are more accurate than the ones you can get by

flipping a coin.

In particular, I've been listening to an unbelievable cacophony of

nonsense about inflation. In the last couple of days I've heard

warnings of the coming round of super-inflation that would match the

1970s. Where do they get these so-called "experts," who are more

idiots than experts. People in the 1970s were survivors of the Great

Depression, so they can't be compared to people today, but mainstream

economists are too stupid to grasp that.

So it was interesting today to read an article of economic analysis

that actually made sense:

"Lulled Into Complacency" - Signposts Of The End Are Everywhere

Authored by Eric Hickman, president of Kessler Investment Advisors, Inc.,

https://www.zerohedge.com/markets/lulle ... everywhere

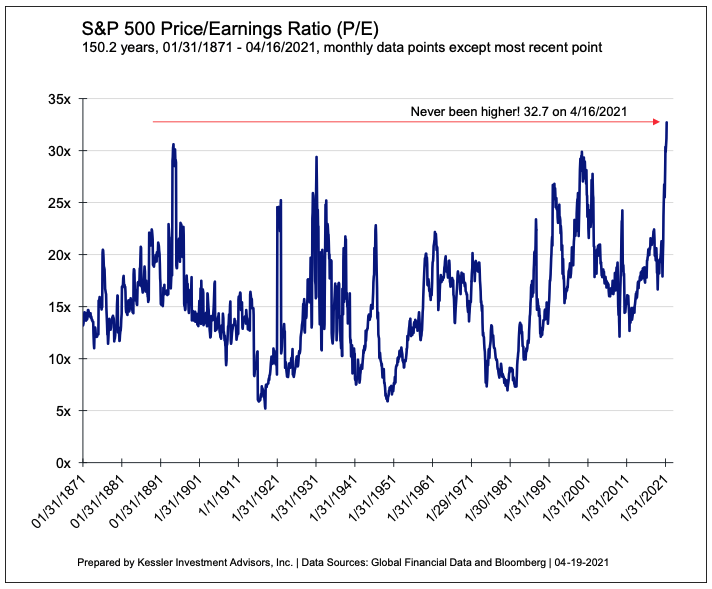

This article analyzes several economic trends back to 1900. It even

gets the Law of Reversion of the Mean right for P/E ratios, although

the text deftly avoids scaring people by mentioning that the long-term

average is 14, but you can see it right from their graph:

This article goes far beyond P/E ratios to numerous other economic

analyses. It's not a full-scale generational analysis, but it's the

closest I've seen.

99% of analyses from mainstream economists are total garbage, as

proven by the fact that they almost always turn out wrong or, at best,

made no forecasts that are more accurate than the ones you can get by

flipping a coin.

In particular, I've been listening to an unbelievable cacophony of

nonsense about inflation. In the last couple of days I've heard

warnings of the coming round of super-inflation that would match the

1970s. Where do they get these so-called "experts," who are more

idiots than experts. People in the 1970s were survivors of the Great

Depression, so they can't be compared to people today, but mainstream

economists are too stupid to grasp that.

So it was interesting today to read an article of economic analysis

that actually made sense:

"Lulled Into Complacency" - Signposts Of The End Are Everywhere

Authored by Eric Hickman, president of Kessler Investment Advisors, Inc.,

https://www.zerohedge.com/markets/lulle ... everywhere

This article analyzes several economic trends back to 1900. It even

gets the Law of Reversion of the Mean right for P/E ratios, although

the text deftly avoids scaring people by mentioning that the long-term

average is 14, but you can see it right from their graph:

- S&P 500 Price/Earnings Ratio (P/E Ratio) - 150.2 years,

1/31/1871 - 04/16/2021, monthly data points

This article goes far beyond P/E ratios to numerous other economic

analyses. It's not a full-scale generational analysis, but it's the

closest I've seen.

Re: Financial topics

** 28-Apr-2021 World View: Conclusions of the 'signposts' article

It's worthwhile to post the conclusions from the article linked in my

previous post:

https://www.zerohedge.com/markets/lulle ... everywhere

But this time is different?

Stock market bulls suggest the stock market will continue rising

because the pandemic will soon be over (I’m not so sure) and developed

economy governments have put enough money into their economies to keep

their stock markets elevated (not sure about that either). Investors

have been lulled into complacency because the stock market has rallied

through every risk thrown its way for more than a decade. It is a

mistake to think this is normal or sustainable.

Some feature of COVID-19 will likely be the stock market’s undoing,

but it doesn’t have to be. Possible candidates include an emerging

market sovereign fiscal crisis, a large hedge-fund/bank blow-up,

fraud, social unrest, or a geopolitical crisis. There is also the

possibility that an inflection point won’t have an identifiable

catalyst, but could happen just from a collective realization that

asset prices reflect optimism extrapolated further into the future

than is realistic. I don’t know when or how, but sentiment will

change; the boom and bust process is as old as civilization.

When it happens, nobody is big enough to stop it coming down. Fiscal

and monetary stimulus is this cycle’s “false idol.” Every cycle has

one – a reason why it can’t come down. Right before the stock market

crash of 1929, Yale economist Irving Fisher said stock prices were in

“what looks like a permanently high plateau.” Portfolio insurance was

the culprit in 1987. In 2000, it was said that the internet was a “new

paradigm” obviating historical comparisons. Before the 2007-2008 stock

market crash, Alan Greenspan, chairman of the Federal Reserve, said

the housing market was too varied geographically to come down at

once. Ben Bernanke, the subsequent chairman of the Federal Reserve,

infamously said that he thought losses to subprime mortgage loans were

“contained.” All of them were wrong.

It's worthwhile to post the conclusions from the article linked in my

previous post:

https://www.zerohedge.com/markets/lulle ... everywhere

But this time is different?

Stock market bulls suggest the stock market will continue rising

because the pandemic will soon be over (I’m not so sure) and developed

economy governments have put enough money into their economies to keep

their stock markets elevated (not sure about that either). Investors

have been lulled into complacency because the stock market has rallied

through every risk thrown its way for more than a decade. It is a

mistake to think this is normal or sustainable.

Some feature of COVID-19 will likely be the stock market’s undoing,

but it doesn’t have to be. Possible candidates include an emerging

market sovereign fiscal crisis, a large hedge-fund/bank blow-up,

fraud, social unrest, or a geopolitical crisis. There is also the

possibility that an inflection point won’t have an identifiable

catalyst, but could happen just from a collective realization that

asset prices reflect optimism extrapolated further into the future

than is realistic. I don’t know when or how, but sentiment will

change; the boom and bust process is as old as civilization.

When it happens, nobody is big enough to stop it coming down. Fiscal

and monetary stimulus is this cycle’s “false idol.” Every cycle has

one – a reason why it can’t come down. Right before the stock market

crash of 1929, Yale economist Irving Fisher said stock prices were in

“what looks like a permanently high plateau.” Portfolio insurance was

the culprit in 1987. In 2000, it was said that the internet was a “new

paradigm” obviating historical comparisons. Before the 2007-2008 stock

market crash, Alan Greenspan, chairman of the Federal Reserve, said

the housing market was too varied geographically to come down at

once. Ben Bernanke, the subsequent chairman of the Federal Reserve,

infamously said that he thought losses to subprime mortgage loans were

“contained.” All of them were wrong.

-

Higgenbotham

- Posts: 8227

- Joined: Wed Sep 24, 2008 11:28 pm

Re: Financial topics

He says homelessness is not something "that the Fed has all the tools for or anything like that." Perhaps the answer to the problem of homelessness is to stop using "all the tools."Q: Hi, Chair Powell. I'm wondering, are you planning to visit the homeless encampment that's near the Fed in Washington that you drive by? Have you been invited? And if you went, what would you be looking to learn there?

MR. POWELL: You know, frankly, I -- yes, I have not had a chance to do it yet, but -- I've been very busy, but I will visit. I don't want to visit at a time of a lot of media attention because I don't want that to be part of the story, but I will -- I will go visit when it's no longer a new story. And you know, I have -- I've met with homeless people many times -- a number of times, anyway, let's say -- and I think it's always good to talk to people and hear what's going on in their lives. What you find out is they're you. They're just us. I mean, they're -- these are people who in many cases had jobs and, you know, they have lives, and they've just -- they have just found themselves in this place.

It's a -- it's a difficult problem, though, you know. There are many, many facets of it. And I'm well aware that this is not something that the Fed has all the tools for or anything like that. But I will do that when the -- when the need arises and when it's not so much, you know, in the public eye.

Q: And is there anything specifically that you would be looking to learn there?

MR. POWELL: Not really. I mean, I think I know what I'll find there. I think you -- you connect with these people, and what you -- again, what you find is they're like you. That could be you. I mean, that could be your sister. That could be, you know, your kid. You always feel that way in that sort of an encounter, and you know, it just is -- it's an important thing to engage in, I think. And I think, you know, we bring that understanding into our lives and, frankly, into our work -- the work that we do, as well.

Yes, the homeless are just us. Except for some reason they weren't able to waddle up to the window for a bailout, or maybe they didn't want to. You have to know how to do the waddle. It's the most critical and in-demand skill in America.

Why $120 billion a month, why not less?Q: Thank you, Mr. Chairman. Since I am last, let me go back to Paul's question, the first question, and ask him -- ask you whether -- not whether you're thinking about thinking of tapering, but why you're not. We're seeing bank lending fall. The markets seem to be operating well. Are you afraid of a taper tantrum? Or is it, as one money manager put it, if you get out of the markets there aren't enough buyers for the treasury debt and so rates would have to go way up? The bottom-line question is: What do we get for $120 billion a month that we couldn't get for less?

MR. POWELL: So, it's not more complicated than this: We articulated the substantial further progress test at our December meeting. And really for the next couple of months we made relatively little progress toward our goals. And there was substantial further progress from December -- from our December meeting. And then vaccination started to get more widespread. The economy reopened. We got a nice job report for March.

It doesn't constitute substantial further progress. It's not close to substantial further progress. We're hopeful we will see along this path a way to that goal. And we believe we will, it just is a question of when. And so when that time -- when the time comes for us to talk about talking about it, we'll do that. But that time is not now. It's -- we're just not -- we're not that far. We've had one great jobs report. It's not enough. You know, we're going to act on actual data, not on our forecast. And we're just going to see more data. It's no more complicated than that.

Q: Well, if you leave rates where they are, doesn't change anything. But does it change anything if you actually tapered a bit? If you spent less would you still get the same effect on the economy?

MR. POWELL: If we bought less -- you're very faint. So if someone has a volume, turn it up. But if we bought less? No, no. I think the effect is proportional to the amount we buy. It's really part of overall accommodative financial conditions. We have tried to create accommodative financial conditions to support activity, and we did that. And we articulated the -- you know, the tests for withdrawing that accommodation.

And we think -- you know, so we're waiting to see those tests to be fulfilled both for asset purchases and for lift off of rates. And, you know, when the tests are fulfilled we'll go ahead. You know, we've done this before. We did it in the last -- after the last crisis. And, you know, we'll do it in maybe -- we'll do it -- as those tests are satisfied, we'll do it. And the only thing that will guide us is, are the tests met? You know, that's what we focus on, is have the macroeconomic conditions that we've articulated, have they been realized? That will be the test for tapering asset purchases and for raising interest rates.

Thank you.

"But if we bought less? No, no. I think the effect is proportional to the amount we buy."

Why $120 billion a month, why not more?

While the periphery breaks down rather slowly at first, the capital cities of the hegemon should collapse suddenly and violently.

Re: Financial topics

** 29-Apr-2021 World View: Jerome Powell and Judas: Damned for all time

edge of a cliff, and he knows that anything he does could be blamed as

the cause of going over the cliff. Powell wants to do the right

thing, but no matter what he does, he's afraid of being "damned for

all time."

I'm a great believer in the concepts of "calling" or "karma" or

"obsession". People (including myself) are driven to do what they

have to do, even when they know that what they're going to do will

lead to disaster. That's a big part of the Greek concept of tragedy.

Have you ever seen the 1960s Broadway musical Jesus Christ Superstar?

In many ways, that play is the story of Judas, and his obsession that

forces him to betray Jesus for 30 pieces of silver. Here's what he

sings just before the betrayal:

no thought at all about my own reward. I really didn't come here of

my own accord. Just don't say I'm ... Damned for all time."

After betraying Jesus, Judas gives the 30 pieces of silver to the

temple, and then kills himself.

I actually feel sorry for Jerome Powell. He knows that we're on theHiggenbotham wrote: Thu Apr 29, 2021 10:48 am > Why $120 billion a month, why not less?

> "But if we bought less? No, no. I think the effect is proportional

> to the amount we buy."

> Why $120 billion a month, why not more?

edge of a cliff, and he knows that anything he does could be blamed as

the cause of going over the cliff. Powell wants to do the right

thing, but no matter what he does, he's afraid of being "damned for

all time."

I'm a great believer in the concepts of "calling" or "karma" or

"obsession". People (including myself) are driven to do what they

have to do, even when they know that what they're going to do will

lead to disaster. That's a big part of the Greek concept of tragedy.

Have you ever seen the 1960s Broadway musical Jesus Christ Superstar?

In many ways, that play is the story of Judas, and his obsession that

forces him to betray Jesus for 30 pieces of silver. Here's what he

sings just before the betrayal:

So I feel sorry for Powell, because he must feel the same way: "I have> Now if I help you, it matters that you see

> These sordid kinda things are coming hard to me.

> It's taken me some time to work out what to do.

> I weighed the whole thing out before I came to you.

> I have no thought at all about my own reward.

> I really didn't come here of my own accord.

> Just don't say I'm ...

> Damned for all time.

>

> I came because I had to; I'm the one who saw.

> Jesus can't control it like he did before.

> And furthermore I know that Jesus thinks so too.

> Jesus wouldn't mind that I was here with you.

> I have no thought at all about my own reward.

> I really didn't come here of my own accord.

> Just don't say I'm ...

> Damned for all time.

>

> Annas, you're a friend, a worldly man and wise.

> Caiaphas, my friend, I know you sympathise.

> Why are we the prophets? Why are we the ones

> Who see the sad solution - know what must be done?

> I have no thought at all about my own reward.

> I really didn't come here of my own accord.

> Just don't say I'm

> Damned for all time.

no thought at all about my own reward. I really didn't come here of

my own accord. Just don't say I'm ... Damned for all time."

After betraying Jesus, Judas gives the 30 pieces of silver to the

temple, and then kills himself.

> Christ, I know you can't hear me,

> But I only did what you wanted me too.

> Christ, I'd sell out the nation,

> For I have been saddled with the murder of you.

> I have been spattered with innocent blood.

> I shall be dragged through the slime and the mud.

> I have been spattered with innocent blood.

> I shall be dragged through the slime and the mud! ...

> When he's cold and dead will he let me be?

> Does he love me too? Does he care for me?

> Oh, Oh!

> My mind is in darkness now.

> My God, I am sick. I've been used,

> And you knew all the time.

> God, I'll never ever ever know why you chose me for your crime.

> Your foul bloody crime.

> God, You have murdered me! You have murdered me, murdered me!

> You have murdered me murdered me murdered me murdered me!

Re: Financial topics

Last nights pabulum for the masses was textbook narrative propaganda.

The only thing spiking today is the self imposed slaughter as Bob Bish

from the Bib Bish body farm cult. Also the current collapse from the border will

grind the locals to dust and already have.

It is a feature for them to take out any pockets of resistance going forward.

They as much as said so this morning in a calibrated press release today.

As we noted the SoCal economy collapsed in plain site since legitimate operations

cannot meet liability's imposed from alleged governances.

It is collapsing real time as as they just pick up bullet ridden corpses at dawn locally now

in a spiritually dead demshevik waste land now.

We are here it more than appears as we warned and noted.

https://mises.org/library/vampire-economy

He had parted company with the German Communist Party because of its growing fealty to Moscow.

Once Hitler came to power, he went underground with the leftist resistance;

he took the name Guenter Reimann and kept it for the rest of his life.

The Potemkin swamp cult will drown you in alleged replacement migration theory needs in Befehl ist Befehl logic.

You are here now. And dominion was given to it. https://www.youtube.com/watch?v=fxz1xI5xxCA

Warned you had been, and seen basically real time to what the sandbox did and was for.

Real time reports from yesterday have been filtered since no edification can come from it

since " Because thou sayest, I am rich, and increased with goods, and have need of nothing;

and knowest not that thou art wretched, and miserable, and poor, and blind, and naked: "

The only thing spiking today is the self imposed slaughter as Bob Bish

from the Bib Bish body farm cult. Also the current collapse from the border will

grind the locals to dust and already have.

It is a feature for them to take out any pockets of resistance going forward.

They as much as said so this morning in a calibrated press release today.

As we noted the SoCal economy collapsed in plain site since legitimate operations

cannot meet liability's imposed from alleged governances.

It is collapsing real time as as they just pick up bullet ridden corpses at dawn locally now

in a spiritually dead demshevik waste land now.

We are here it more than appears as we warned and noted.

https://mises.org/library/vampire-economy

He had parted company with the German Communist Party because of its growing fealty to Moscow.

Once Hitler came to power, he went underground with the leftist resistance;

he took the name Guenter Reimann and kept it for the rest of his life.

The Potemkin swamp cult will drown you in alleged replacement migration theory needs in Befehl ist Befehl logic.

You are here now. And dominion was given to it. https://www.youtube.com/watch?v=fxz1xI5xxCA

Warned you had been, and seen basically real time to what the sandbox did and was for.

Real time reports from yesterday have been filtered since no edification can come from it

since " Because thou sayest, I am rich, and increased with goods, and have need of nothing;

and knowest not that thou art wretched, and miserable, and poor, and blind, and naked: "

-

Higgenbotham

- Posts: 8227

- Joined: Wed Sep 24, 2008 11:28 pm

Re: Financial topics

John wrote: Thu Apr 29, 2021 11:28 am ** 29-Apr-2021 World View: Jerome Powell and Judas: Damned for all time

I actually feel sorry for Jerome Powell. He knows that we're on the

edge of a cliff, and he knows that anything he does could be blamed as

the cause of going over the cliff. Powell wants to do the right

thing, but no matter what he does, he's afraid of being "damned for

all time."

http://www.generationaldynamics.com/pg/ ... rnanke.htmBen S. Bernanke: The man without agony

Bernanke and Greenspan are as different as night and day, despite what the pundits say. (29-Oct-2005)

Summary

Ben S. Bernanke, President Bush's nominee for the new Fed Chairman, is completely different from the man he'll be replacing, Alan Greenspan. Nowhere is the difference so apparent as when you contrast Bernanke's "What me worry?" attitude toward economic bubbles with Greenspan's genuine agony over the fact that his gut is telling him that we're headed for a major financial crisis.

Possibly what bothers me most about Ben S. Bernanke is that I fail to detect in him any of the agony that has characterized Alan Greenspan’s speeches in the last year.

There are many things - race, religion, etc. - that are irrelevant to predicting how a Fed chairman will conduct policy. But the generation into which a man is born is very relevant.

We can see that right away in their policy priorities.

A generation apart

Greenspan was born in 1926, and grew up surrounded by massive starvation and homelessness in the Great Depression, so his priority at the Fed has been to contain the damage from the 1990s bubble.

Bernanke was born in 1953 and grew up during the 1950s, when America had already defeated the Depression and defeated the Nazis, and no goal was out of reach. He was in college in the 1970s when high inflation was the major problem, so naturally inflation is his highest priority policy issue today.

Bernanke doesn’t worry about bubbles, because to him those were all fixed in the 1930s, and now they always take care of themselves.

Although Jerome Powell was born in 1953, I would characterize him as a man with agony. But there seems to be a difference between him and Greenspan. My best guess is that Powell fears a replay of the second half of 2018 or the first half of 2020, only worse. Greenspan feared a replay of the Great Depression.

Through 2005, Greenspan has seemed to me to be increasingly in agony, as he’s seen the stock bubble of 2000 morph into a stock bubble and a housing bubble. This was beginning to look all too familiar to him; things he hadn’t seen since his childhood. It’s not surprising that Greenspan privately told France’s Finance Minister last month that “the United States has lost control of their budget.”

His public remarks were at their starkest in his “swan song” Fed speech at the end of August.

In that speech he commented favorably on the economy’s flexibility because it encourages investor risk, but warned about the stock market and housing bubbles, and added:

"To some extent, those higher [stock and housing] values may be reflecting the increased flexibility and resilience of our economy. But what [investors] perceive as newly abundant liquidity can readily disappear. Any onset of increased investor caution elevates risk premiums and, as a consequence, lowers asset values and promotes the liquidation of the debt that supported higher asset prices. This is the reason that history has not dealt kindly with the aftermath of protracted periods of low risk premiums."

History has not dealt kindly ...

When Greenspan says that “history has not dealt kindly,” he’s referring to the 1930s Depression, and he’s telling us that he thinks it’s going to happen again. Just reading his words you can almost hear the agony in his voice, as he realizes that the horrors he suffered as a boy are going to happen again – and that he’ll be blamed for it, and that it will be his legacy.

The stock market today is priced at Dow 10,300, but the underlying book value of the market is Dow 4,500 according to my computations – and according to computations performed using a different method by analyst Adam Barth in an article appearing in the July 11, 2005 issue of Barron’s.

So the market is priced at 228 per cent of book value today, which is about where it was just before the 1929 panic. Bernanke undoubtedly believes that a new panic today wouldn't do any more harm than the 1987 panic that he's old enough to remember, but the market was at 102 per cent of book value at that time, so it's not surprising that the market recovered quickly then. A panic today would be as bad as 1929.

While the periphery breaks down rather slowly at first, the capital cities of the hegemon should collapse suddenly and violently.

-

Higgenbotham

- Posts: 8227

- Joined: Wed Sep 24, 2008 11:28 pm

Re: Financial topics

Higgenbotham wrote: Fri Apr 30, 2021 12:44 amJohn wrote:Through 2005, Greenspan has seemed to me to be increasingly in agony, as he’s seen the stock bubble of 2000 morph into a stock bubble and a housing bubble. This was beginning to look all too familiar to him; things he hadn’t seen since his childhood. It’s not surprising that Greenspan privately told France’s Finance Minister last month that “the United States has lost control of their budget.”

His public remarks were at their starkest in his “swan song” Fed speech at the end of August.

In that speech he commented favorably on the economy’s flexibility because it encourages investor risk, but warned about the stock market and housing bubbles, and added:

"To some extent, those higher [stock and housing] values may be reflecting the increased flexibility and resilience of our economy. But what [investors] perceive as newly abundant liquidity can readily disappear. Any onset of increased investor caution elevates risk premiums and, as a consequence, lowers asset values and promotes the liquidation of the debt that supported higher asset prices. This is the reason that history has not dealt kindly with the aftermath of protracted periods of low risk premiums."

History has not dealt kindly ...

When Greenspan says that “history has not dealt kindly,” he’s referring to the 1930s Depression, and he’s telling us that he thinks it’s going to happen again. Just reading his words you can almost hear the agony in his voice, as he realizes that the horrors he suffered as a boy are going to happen again – and that he’ll be blamed for it, and that it will be his legacy.

The stock market today is priced at Dow 10,300, but the underlying book value of the market is Dow 4,500 according to my computations – and according to computations performed using a different method by analyst Adam Barth in an article appearing in the July 11, 2005 issue of Barron’s.

So the market is priced at 228 per cent of book value today, which is about where it was just before the 1929 panic. Bernanke undoubtedly believes that a new panic today wouldn't do any more harm than the 1987 panic that he's old enough to remember, but the market was at 102 per cent of book value at that time, so it's not surprising that the market recovered quickly then. A panic today would be as bad as 1929.

https://twitter.com/hussmanjp/status/13 ... 48162?s=20

The difference between 1929, 2000, and today is the 10 year is yielding about 1.6%, so while the equity risk premium is about the same today as it was in 1929 and 2000, the expected return on stocks will be even lower today.

While the periphery breaks down rather slowly at first, the capital cities of the hegemon should collapse suddenly and violently.

Who is online

Users browsing this forum: Bing [Bot], Google [Bot] and 2 guests